Key Highlights

- SK Hynix claimed the position as South Korea’s largest publicly traded corporation by market capitalization, reaching $1.35 trillion

- Shares have skyrocketed over 340% throughout the year, fueled by explosive growth in high-bandwidth memory (HBM) chip sales for artificial intelligence applications

- The company commands 61% of the worldwide HBM market, significantly outpacing Samsung’s 17% and Micron’s 21% shares

- Samsung maintained market leadership since 2000, though it contends that including preferred shares would place its total valuation near 2,252 trillion won

- Plans are underway for SK Hynix to pursue a Nasdaq listing in the United States to expand its shareholder reach

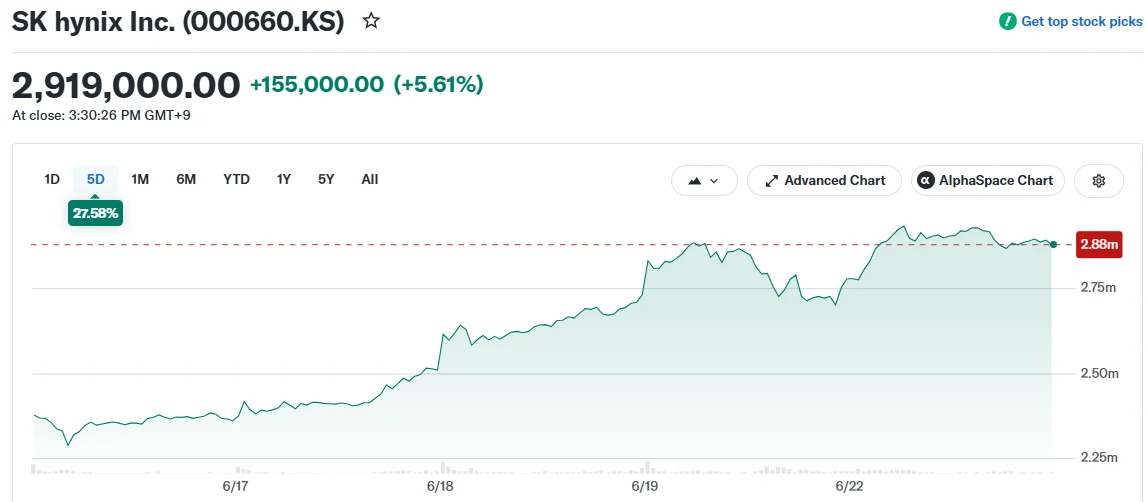

SK Hynix shares jumped 5.7% during Monday’s trading session, elevating its total market value to 2,082.5 trillion won ($1.35 trillion) and narrowly surpassing Samsung Electronics — which climbed a modest 0.4% — marking a historic shift in market positioning.

Samsung has occupied the number one position for nearly a quarter-century. The margin separating these technology titans remains extremely narrow, with Samsung maintaining that factoring in its preferred stock category would elevate its total market capitalization to approximately 2,252 trillion won.

This achievement represents the culmination of an extraordinary performance by SK Hynix, whose shares have surged more than 340% year-to-date.

The driving force behind this spectacular rally centers on HBM technology — advanced high-bandwidth memory chips engineered with vertical stacking architecture to enable superior data transfer speeds while reducing power requirements. These specialized components serve as critical building blocks within AI processors manufactured by Nvidia and deployed by major technology firms including Alphabet’s Google.

Different from conventional DRAM memory products, HBM chips are deeply integrated with AI computing infrastructure. This integration establishes significant competitive moats and provides manufacturers with pricing leverage that commodity memory producers historically lacked. SK Hynix dominates 61% of the worldwide HBM market. Samsung captures 17%, while Micron holds 21%.

Remarkable Transformation from Financial Crisis to $1.35 Trillion Giant

The corporate resurrection narrative behind this achievement demands attention. Back in 2002, the company then operating as Hynix Semiconductor teetered on the edge of bankruptcy, nearly acquired by Micron following a crushing debt crisis. When negotiations collapsed, creditors assumed control for approximately ten years. Share prices plummeted to 135 won by 2003 — effectively penny stock territory.

During 2023, a severe memory market contraction inflicted substantial damage. SK Hynix reported an annual operating deficit totaling 7.73 trillion won during that challenging period.

Despite market headwinds, the company maintained aggressive HBM technology investments throughout the slump — a strategic gamble that ultimately delivered exceptional returns. By 2024, it generated unprecedented operating profits of 23.5 trillion won as cloud infrastructure investments from Microsoft, Google, and Meta intensified dramatically.

SK Group Chairman Chey Tae-won, who championed the controversial Hynix acquisition against fierce internal resistance, articulated his strategic vision in a recently published book from January.

“What I really wanted to accomplish when we acquired Hynix was to transform it from a commodity memory producer into a mainstream semiconductor company whose products are indispensable,” he said.

He added: “In the past, it did not matter whether memory came from Hynix, Samsung or Micron. HBM is different. If SK Hynix’s HBM is replaced with another product, the AI system may not function properly.”

Samsung Faces Mounting Pressure in DRAM Manufacturing

The competitive dynamics extend beyond simple market capitalization comparisons. Samsung’s longstanding leadership in DRAM manufacturing capacity faces mounting challenges.

Bank of America projects SK Hynix’s monthly DRAM production capacity will hit approximately 589,000 wafers during the current year, compared to Samsung’s roughly 691,000 wafers. However, SK Hynix plans aggressive capacity expansion of 38% spanning 2025 through 2028, substantially exceeding Samsung’s projected 17.5% growth trajectory.

By 2028, this expansion strategy would shrink the manufacturing capacity differential to less than 10%, down dramatically from the current 23% gap in 2025.

“Previously, the difference in manufacturing scale meant there was simply no way for rivals to close the profitability gap with Samsung,” said Kim Sunwoo, senior analyst at Meritz Securities.

SK Hynix is also reportedly advancing preparations for a secondary listing on the Nasdaq exchange, a strategic move designed to enhance visibility and accessibility among international institutional investors.