Quick Summary

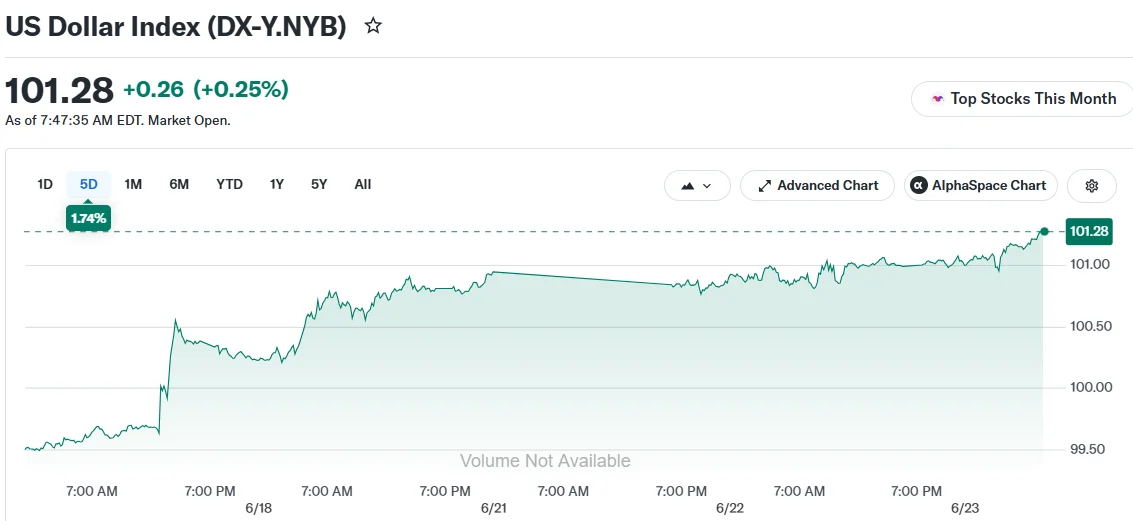

- The US Dollar Index surged to 101.25, marking its strongest performance in more than twelve months

- Market expectations now reflect an 80–85% probability of a Federal Reserve rate increase by fall 2025

- Japan’s currency is trading near its most vulnerable position since 1986, sparking intervention speculation

- Political upheaval in Britain following Prime Minister Keir Starmer’s resignation has weighed on sterling

- The euro dropped to levels not seen since August 2025 following dovish commentary from ECB President Lagarde

The greenback surged to a fresh 12-month peak on Tuesday as market participants ramped up expectations that the Federal Reserve will implement an interest rate increase before year-end. The Dollar Index reached 101.25, representing its strongest level since May of last year.

Futures markets tied to Fed funds rates currently indicate approximately 80 to 85% odds of a 25-basis-point rate increase arriving by September or October. Major financial institutions including BofA Global Research and Deutsche Bank have adjusted their outlooks, abandoning previous predictions of unchanged policy in favor of anticipating a hike within the coming months.

“At this moment, the dollar is reflecting expectations of elevated rates and strengthening accordingly,” stated Tommy von Bromsen, foreign exchange strategist at Handelsbanken.

Persistent geopolitical instability stemming from unresolved conflicts in the Middle East is providing additional tailwinds for dollar strength, von Bromsen noted.

Japanese Currency Flirts with Four-Decade Low

The Japanese yen continues trading in precarious territory. The currency momentarily touched 161.93 against the dollar during Monday’s session, and any breach above 161.96 would represent its feeblest showing since the mid-1980s.

Traders remain vigilant for potential market intervention by Tokyo officials. Japanese authorities deployed tens of billions of dollars during late April and early May attempting to support their currency, though these measures yielded only temporary relief.

The Bank of Japan implemented an interest rate increase last week while indicating additional monetary tightening lies ahead. Despite this hawkish pivot, the yen has continued its descent, hampered by the substantial interest rate differential between the United States and Japan.

Japanese Finance Minister Satsuki Katayama conducted discussions with US Treasury Secretary Scott Bessent on Monday. Their conversation centered on coordinated policy approaches addressing the yen’s weakness, including the possibility of foreign exchange market intervention.

Sterling Slides on Political Turmoil, Euro Weakens

The British pound retreated 0.2 to 0.3% on Tuesday following UK Prime Minister Keir Starmer‘s resignation announcement, injecting fresh political instability into British financial markets. Health Minister Wes Streeting publicly endorsed Andy Burnham as a successor, a development market observers suggest could limit uncertainty surrounding the leadership succession.

“Given Streeting’s readiness to support Burnham, this period of uncertainty will likely prove short-lived,” observed Michael Pfister, foreign exchange analyst at Commerzbank.

The euro likewise declined, sliding to $1.1395, representing its weakest reading since August 2025. ECB President Christine Lagarde minimized concerns about secondary inflation effects during Monday remarks, while fresh data revealed eurozone private sector contraction extending into a third consecutive month in June.

The Australian dollar decreased 0.7 to 0.8%, touching its most depressed level since April.

Market participants are now focusing intently on forthcoming US economic releases. Wednesday brings the May PCE price index, which serves as the Federal Reserve’s primary inflation measurement. June PMI figures and a revised first-quarter GDP estimate are also scheduled for release this week. These data points could prove decisive in determining whether the dollar’s upward momentum has additional runway.