Key Takeaways

- The Dow Jones Industrial Average surged more than 500 points (approximately 1%) on Thursday, June 4, even as the S&P 500 and Nasdaq declined

- Broadcom stock plummeted over 14% following disappointing guidance for AI chip revenue that missed investor forecasts

- The iShares Semiconductor ETF tumbled 4.4%, weighing heavily on technology shares

- Congress voted to terminate military operations against Iran, following recent tensions

- SpaceX disclosed intentions for a massive $75 billion public offering through regulatory documents

American equity markets experienced a notable divergence on Thursday, with traditional industrial stocks rallying while technology shares retreated.

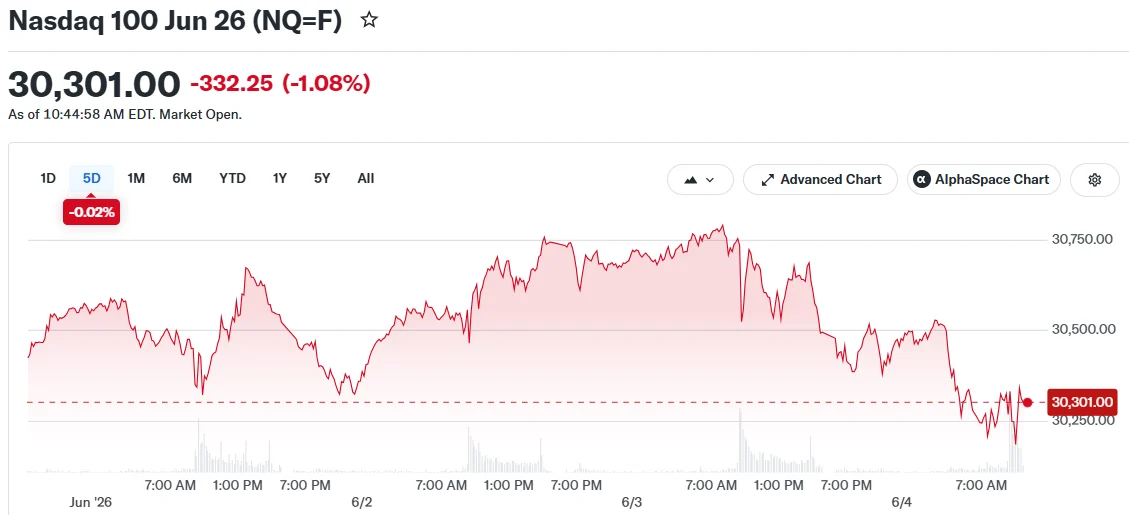

The Dow Jones Industrial Average advanced more than 500 points, representing approximately 1% growth. Meanwhile, the S&P 500 declined roughly 0.2–0.3%, while the Nasdaq dropped over 1%.

This market divergence was particularly noteworthy. The majority of individual stocks within both the Dow and S&P 500 were actually gaining ground. However, severe declines among semiconductor companies exerted enough downward pressure to offset broader market strength.

Broadcom’s Results Spark Technology Sector Retreat

Broadcom stock tumbled more than 14% on Thursday following the semiconductor giant’s AI chip revenue projection, which disappointed market participants.

While Broadcom’s quarterly results exceeded analyst estimates, the company’s forward guidance failed to meet the elevated expectations built up during its impressive year-long rally.

“All it takes is one company to at least temporarily wreck the party,” said Bespoke Investment Group co-founder Paul Hickey. “Yesterday, the party pooper was Broadcom.”

The iShares Semiconductor ETF suffered a 4.4% decline during the session. Other semiconductor manufacturers including Micron and Sandisk also posted losses.

Nvidia, representing the sole chip manufacturer in the Dow, demonstrated relative resilience with only a 0.3% decrease.

The technology-concentrated Nasdaq had posted consecutive daily gains for approximately two weeks before Thursday’s reversal. Market strategists had cautioned that the advance was being driven by an increasingly narrow group of stocks — a dynamic that can create vulnerability for major indexes.

Geopolitical Developments, Employment Data, and SpaceX IPO Update

Investors also digested significant geopolitical news. On Wednesday, the House of Representatives approved legislation to conclude U.S. military engagement with Iran. This congressional action followed a major escalation earlier in the week — representing the most serious flare-up since a ceasefire agreement was established in April.

Oil prices retreated on Thursday as President Trump outlined potential terms for a ceasefire agreement. The U.S. dollar and Treasury yields also moderated.

With Friday’s May employment report approaching, market participants received two Thursday labor market indicators: weekly initial jobless claims from the Bureau of Labor Statistics and corporate layoff statistics from Challenger, Gray & Christmas. Holiday-week factors contributed to elevated jobless claims.

Separately, SpaceX revealed through a fresh SEC filing its intention to pursue a $75 billion initial public offering — positioning it among the largest IPOs in history.

Corporate earnings season progressed with anticipated reports from Ciena Corporation, Lululemon Athletica, and DocuSign scheduled for Thursday.

Earlier during the trading week, Alphabet’s equity issuance strengthened projections that artificial intelligence investment would maintain momentum. However, following an extended technology sector rally, Broadcom’s underwhelming forecast proved sufficient to undermine investor conviction.

Both the S&P 500 and Nasdaq were tracking toward a consecutive second session of declines as the afternoon trading period approached.