Key Highlights

- The yellow metal remains confined within a $4,400–$4,600/oz band for approximately ten trading sessions

- Diplomatic negotiations between Washington and Tehran persist without meaningful progress

- Rising inflation expectations are driving market participants to anticipate Federal Reserve tightening by year-end

- Monetary policy and currency strength now exert greater influence on gold than conflict-related factors

- Other precious metals including silver and platinum experienced declines mid-week

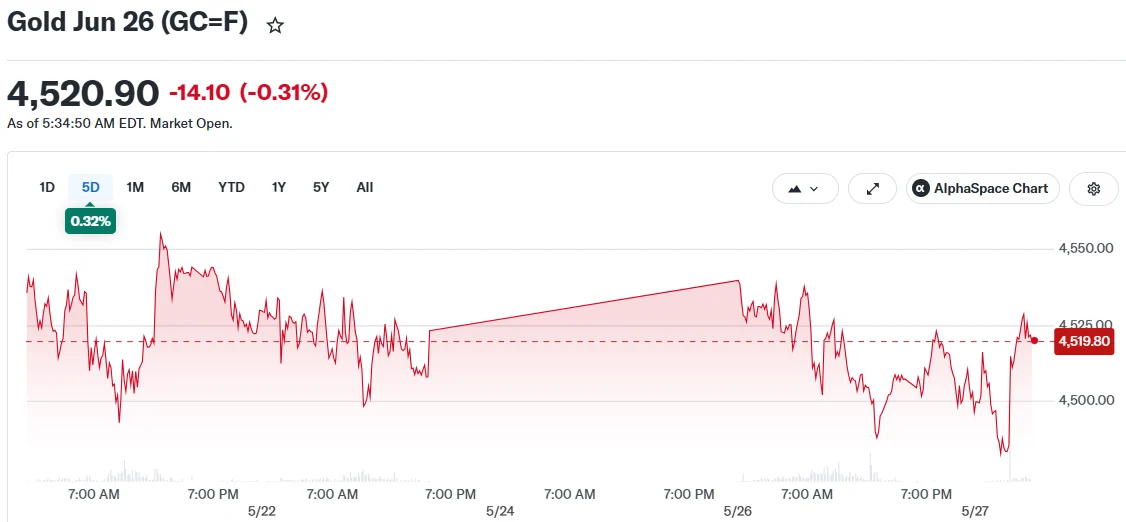

The precious metal market finds itself in a holding pattern around the $4,500 per ounce level as market participants monitor ongoing diplomatic efforts between the United States and Iran. The yellow metal has been unable to escape its constrained price channel.

During Asian trading hours on Wednesday, spot gold stood at $4,505.93 per ounce. Gold futures registered a modest 0.1% advance to reach $4,539.01 per ounce. However, as European markets opened, futures reversed course, declining 0.4% to settle at $4,483.80.

For roughly ten consecutive days, the precious metal has remained trapped within a $4,400 to $4,600 corridor. Market participants are receiving conflicting signals from both Middle Eastern developments and economic indicators.

According to reporting by Al Jazeera, indirect diplomatic channels between Washington and Tehran remain active. Nevertheless, significant disagreements persist on critical matters including Tehran’s nuclear program and strategic control over the Strait of Hormuz shipping lane.

Early in the trading week, American military forces conducted operations targeting locations in southern Iran. This development triggered a Tuesday selloff before prices partially recovered.

Rising Price Pressures Challenge Gold’s Momentum

The primary headwind confronting gold at present stems from inflation concerns rather than military conflict. Recent economic releases revealed energy-fueled price acceleration during the March and April period.

This development has prompted financial markets to anticipate potential interest rate increases from central banking authorities, particularly the Federal Reserve. Elevated interest rates typically create unfavorable conditions for gold ownership due to increased opportunity costs.

According to CME Fedwatch data, financial markets are currently assigning approximately a 40% probability to a Federal Reserve rate increase by December.

Analysts at ANZ noted in their market commentary that heightened inflation prospects have elevated market expectations for monetary tightening. They emphasized that a sustainable gold rally would require the metal to decouple from its present correlation with risk-oriented assets.

Simon-Peter Massabni from XS.com observed that gold’s traditional safe-haven characteristics are facing scrutiny. He highlighted that monetary policy direction, dollar strength, and market liquidity conditions have emerged as more powerful price drivers than geopolitical or military developments.

Traditional Safe-Haven Dynamics Face Scrutiny

Financial markets appear to be prioritizing inflation concerns over immediate geopolitical risks. The conventional wisdom that gold rallies during crisis periods is being challenged.

Since the escalation of US-Iran hostilities, gold has delivered disappointing returns relative to historical patterns. The metal’s defensive appeal has been diminished by mounting rate increase speculation.

Additional precious metals also experienced downward pressure on Wednesday. Spot silver retreated 0.3% to $76.79 per ounce. Spot platinum decreased 0.9% to reach $1,948.63 per ounce.

Market attention now shifts to crucial American economic releases scheduled for this week. Thursday will bring a revised first-quarter GDP estimate alongside the PCE price index, which serves as the Federal Reserve’s preferred inflation gauge.

These forthcoming data points possess the potential to reshape interest rate expectations and catalyze significant gold price movement in either direction.