Key Takeaways

- Precious metal tumbled beneath $4,000 per ounce, marking the sharpest monthly decline since the 2008 financial crisis

- Bullion has retreated approximately 30% from its January high of $5,589

- Capital flows shifted dramatically from precious metals to technology and semiconductor equities, with chip indices soaring over 100% year-to-date

- Federal Reserve policy expectations reversed course toward rate increases, pressuring assets without yield

- Cryptocurrency markets mirrored the decline, with Bitcoin dropping under $60,000, representing a 53% correction from October peaks

The precious metal market faces mounting headwinds from multiple fronts. Concerns about persistent inflation, an increasingly hawkish central bank stance, and extraordinary gains in technology equities have converged to drive bullion deep into bear market conditions.

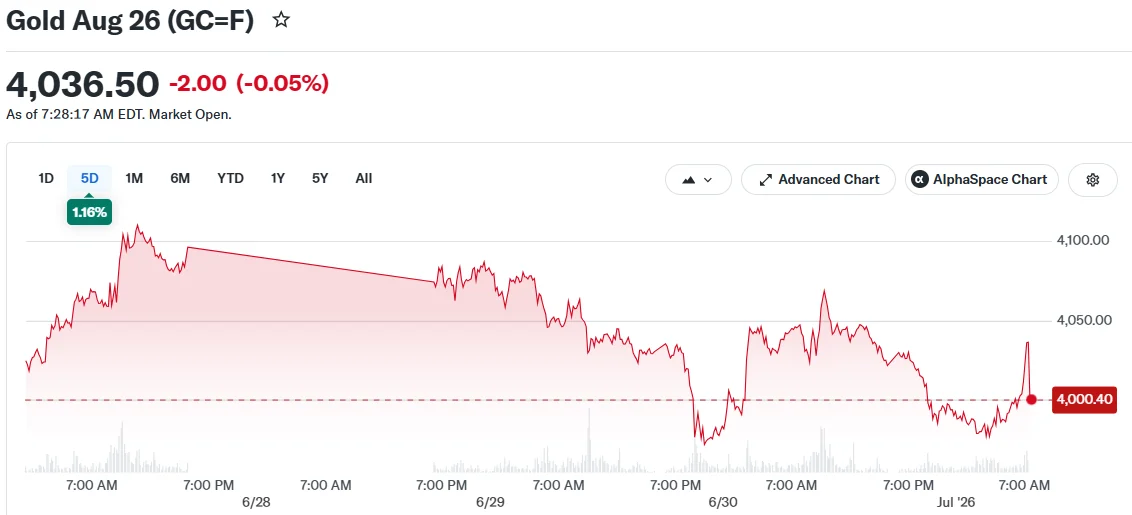

Spot pricing for the yellow metal descended to approximately $3,994 per ounce midweek, breaching the psychologically significant $4,000 threshold for just the second occasion since November. Futures contracts similarly declined, settling around $4,008.

Historic Quarterly Downturn for Precious Metals

Gold experienced approximately a 14% decline during the second quarter, representing its most severe quarterly contraction since 2013. June specifically witnessed an 11.7% depreciation, the most dramatic single-month loss recorded since 2008.

The acceleration in selling intensified following the Federal Reserve’s June policy session, during which multiple committee members indicated openness to implementing at least one rate increase in 2026. This marked a dramatic departure from year-beginning forecasts that anticipated monetary easing.

Newly appointed Fed Chair Kevin Warsh underscored this hawkish positioning during his inaugural policy gathering, stressing the central bank’s commitment to restoring inflation to the 2% objective. Warsh’s scheduled appearance at a European Central Bank forum in Sintra, Portugal later Wednesday has captured significant market attention.

Elevated interest rates diminish gold’s attractiveness by increasing the opportunity cost associated with maintaining positions in assets that generate no income. The appreciating dollar, strengthened by rate projections and perceptions that America faces limited exposure to energy disruptions from Middle East conflicts, has compounded the pressure.

Worldwide gold exchange-traded fund inventories have contracted roughly 1.5% since year-start. The World Gold Council observed that May witnessed flows diminishing “to a trickle,” as capital managers reallocated resources toward technology equities to maintain benchmark performance.

Technology Sector Boom Redirects Investment Capital

The PHLX semiconductor benchmark has surged beyond 100% since January and delivered its strongest quarterly showing on record, climbing approximately 88% during the three-month period concluding in June. Such exceptional returns have redirected billions in capital away from precious metal allocations.

Alternative precious metals encountered similar challenges. Spot silver decreased 0.5% to $58.29 per ounce, while platinum registered modest gains to $1,556.49.

Bitcoin tracked gold’s downward trajectory, slipping beneath $60,000. The digital asset has surrendered more than 53% from its record peak of $126,198 established in October, including a 13% second-quarter loss and 32% year-to-date decline through 2026.

Not all market observers maintain pessimistic long-term projections for bullion. Central banking institutions accumulated 244 tons during the opening quarter, and Chinese monetary authorities have maintained consecutive monthly purchases for 19 months. Approximately 84% of central banks polled by the World Gold Council anticipate expanding their holdings throughout the upcoming five-year period.

ING strategist Ewa Manthey projects gold averaging $4,300 during the third quarter, advancing toward roughly $4,600 in the fourth period. UBS analysts characterize the bull market as “on pause, rather than over,” suggesting the $4,000 level should attract value-oriented long-term purchasers.

Fresh employment statistics are scheduled for Wednesday release, with comprehensive U.S. jobs figures for June arriving Thursday.