Key Takeaways

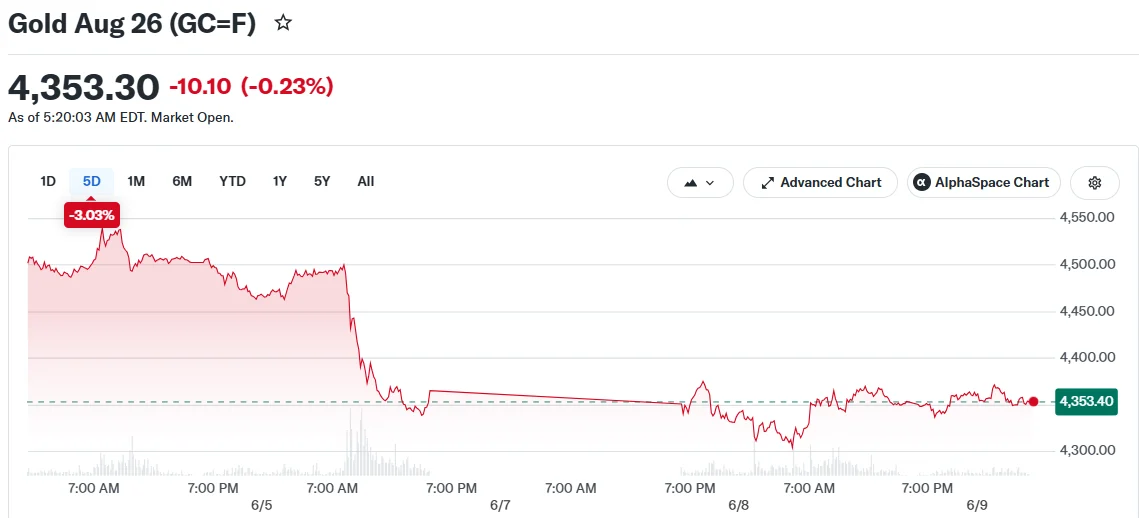

- The precious metal is trading close to an 11-week low between $4,328 and $4,333 per ounce following a nearly 5% decline last week.

- A ceasefire agreement between Iran and Israel has reduced geopolitical tensions that previously supported safe-haven demand.

- Robust employment figures from the United States have strengthened the case for the Federal Reserve maintaining elevated interest rates.

- Current market sentiment suggests approximately a 70% probability of a Fed rate increase by year-end.

- Wednesday’s U.S. inflation report and Thursday’s producer price data are expected to influence the precious metal’s near-term trajectory.

The yellow metal has faced significant headwinds recently. Prices fell to their lowest point since March 23 during last week’s trading session, declining nearly 5% amid the most severe escalation of Middle Eastern conflict since the April truce took effect.

During Tuesday’s Asian trading hours, spot gold was quoted between $4,328 and $4,333 per ounce. U.S. Gold Futures saw a marginal decline, settling around $4,358 per ounce.

The recent selloff was primarily triggered by last week’s stronger-than-anticipated U.S. employment statistics. These figures have bolstered the outlook that the Federal Reserve might maintain its restrictive monetary policy stance for an extended period, which generally pressures gold prices since the metal generates no income.

Current market positioning indicates around a 70% likelihood of a Fed interest rate hike occurring before December.

The U.S. Dollar Index climbed to its highest level in two months before retreating 0.2% on Tuesday, creating additional headwinds for commodities priced in dollars, including gold.

Middle East Hostilities Cool Down

Gold received modest support following an agreement between Iran and Israel to cease hostilities after weekend violence.

U.S. President Donald Trump stated Monday evening that America was approaching a “total victory” declaration regarding the Iran situation and anticipated a significant decline in oil prices.

The ongoing conflict, now entering its fourth month, has interrupted energy transportation through the Strait of Hormuz, elevated oil prices, and sparked concerns about worldwide inflation.

These inflationary pressures have worked against gold’s appeal. Elevated oil prices have maintained higher Treasury yields and dollar strength, diminishing the attractiveness of non-interest-bearing assets.

On Monday, Yemen’s Iranian-backed Houthis declared a blockade targeting Israeli vessels in the Red Sea, introducing another element of regional instability.

Rhona O’Connell, head of market analysis at StoneX Group, indicated that fundamental issues surrounding the conflict remain “unresolved” and mentioned the firm was monitoring for potential value-driven buying opportunities.

Inflation Data Takes Center Stage

Market participants are now focused on Wednesday’s U.S. consumer price index release, with producer price statistics following on Thursday.

These economic indicators will provide crucial insight into whether elevated energy costs are contributing to broader inflationary pressures. The outcomes could significantly alter Federal Reserve policy expectations and impact gold’s direction.

Silver climbed approximately 0.4–0.5% to reach about $68 per ounce. Platinum increased 0.3% to $1,767 per ounce. Copper posted gains across both London Metal Exchange and U.S. futures trading.

Gold continues to navigate between competing dynamics: potential further de-escalation in Middle East geopolitical risks on one hand, and sustained pressure from elevated U.S. interest rate expectations on the other.