Key Takeaways

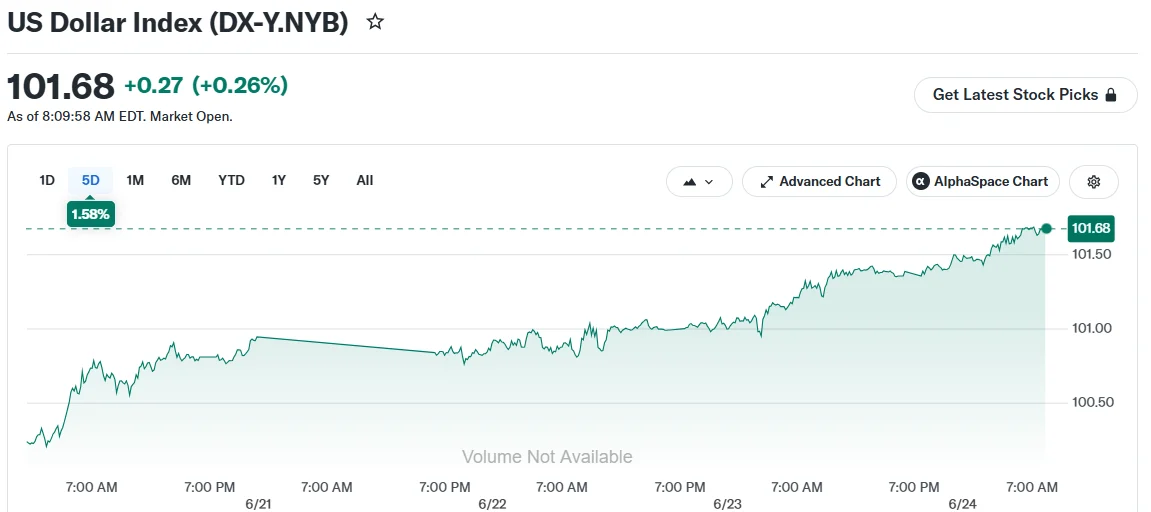

- The greenback reached 101.63 on the U.S. Dollar Index, marking its strongest performance since May 2025, with year-to-date gains approaching 3.3%.

- Investor flight to safety intensified following a massive technology sector collapse that eliminated over $1.3 trillion in market capitalization.

- Market participants anticipate at least two additional Federal Reserve interest rate increases in 2026, with September seeing 60% probability.

- Major currencies faced downward pressure: the euro reached 12-month lows, while the yen traded near four-decade weakness levels.

- Dollar appreciation threatens S&P 500 corporate profits, particularly among Magnificent Seven firms generating half their revenues internationally.

A devastating technology sector collapse that eliminated more than $1.3 trillion across two trading days drove investors into the U.S. dollar on Wednesday, propelling America’s currency to its strongest position in over twelve months.

The U.S. Dollar Index reached 101.63 during trading hours, representing a 0.2% daily advance. Year-to-date performance now stands at approximately 3.3%. Tuesday’s peak of 101.69 marked the currency’s most robust reading since May 2025.

The currency’s ascent persisted despite a Wednesday morning rebound in American equities. This resilience suggests the dollar rally extends beyond immediate technology sector concerns.

Federal Reserve Policy Bolsters Currency Momentum

Market pricing reflects expectations for a minimum of two additional Federal Reserve rate increases before year-end. Futures markets indicate 60% probability for a September adjustment and approximately 40% likelihood for a July move.

Kevin Warsh, recently appointed Fed Chair, has communicated a restrictive monetary policy stance. This positioning has elevated speculative dollar holdings to levels not witnessed since early in the previous year, according to LPL Financial data.

Technical market observers indicate that sustained trading above 100.64 could propel the index toward 105. Downside support exists near the 20-day moving average around 99.75.

Persistent inflationary pressures combined with robust domestic consumption patterns maintain the pathway for continued rate increases, enhancing the dollar’s appeal among international investors pursuing yield opportunities.

International Currencies Face Headwinds

The euro declined for its third consecutive session, touching its weakest level against the dollar in more than twelve months. The European Central Bank faces the dual challenge of lingering inflation stemming from a recent three-month conflict alongside emerging signs of economic deceleration.

The Japanese yen remained positioned near 40-year weakness levels. The dollar-yen exchange rate advanced 0.1% to 161.70. Japan’s Ministry of Finance has deployed approximately $72 billion in foreign exchange intervention efforts. Japanese finance officials engaged in discussions with U.S. Treasury Secretary Scott Bessent during the week.

The Bank of Japan implemented a rate increase to 1.0% last week, representing the highest level since the mid-1990s, yet the yen has failed to mount a sustainable recovery.

China’s yuan also experienced weakness after the People’s Bank of China established its daily reference rate lower for a fourth consecutive session. The Australian dollar remained unchanged despite inflation readings exceeding forecasts.

Implications for American Equity Markets

Dollar strength presents challenges for corporations with substantial international revenue exposure. Approximately one-third of S&P 500 revenues originate from foreign markets.

Among the Magnificent Seven technology giants, that proportion increases to roughly 50%. Nvidia generates 53% of revenues internationally. Meta derives nearly two-thirds of revenues from markets outside the United States.

When international profits undergo conversion to dollars, an appreciating greenback diminishes their reported value. This dynamic could pressure earnings projections, which currently anticipate second-quarter expansion of 23% and full-year growth exceeding 25%.