Key Highlights

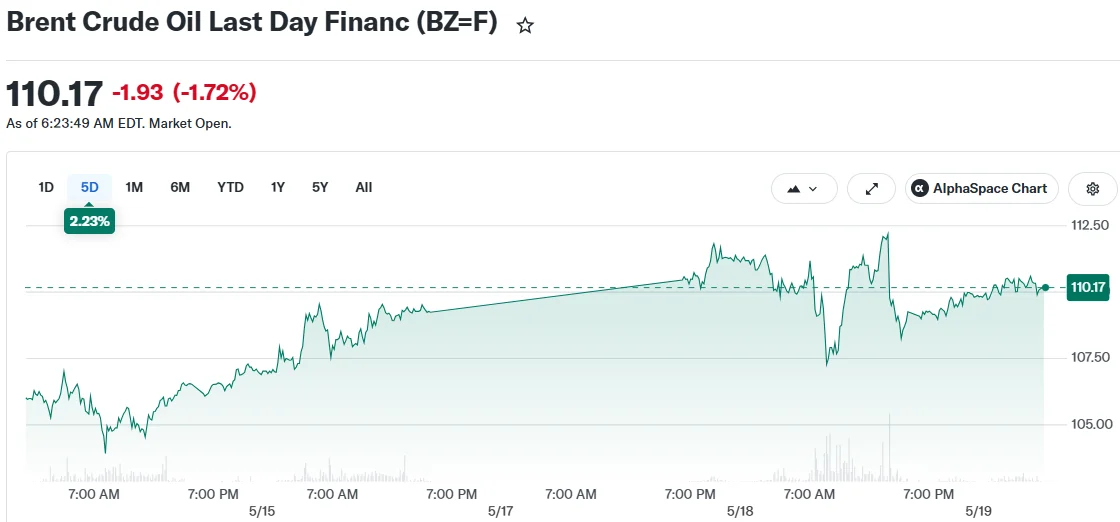

- Brent crude declined 1.5% to $110.39 following Trump’s announcement of postponed Iran military action

- Gulf nations including Saudi Arabia, Qatar, and UAE urged Washington to delay strikes amid active diplomatic talks

- Crude benchmarks have surged more than 80% year-to-date and 20% over the last 30 days

- Iran’s Kharg Island export terminal remains inactive for over 10 days due to US naval presence

- Washington rolled over its exemption for Russian crude currently aboard tankers for an additional month

Crude oil markets experienced a pullback Tuesday following President Donald Trump’s declaration that he postponed planned military operations against Iran after receiving requests from regional allies.

Brent crude decreased 1.5% to settle at $110.39 per barrel. West Texas Intermediate declined 0.7% to $103.64. Despite the retreat, both benchmarks maintain substantial gains from their year-opening levels.

Regional Leaders Persuade Trump to Delay Military Operations

Through a social media statement, Trump revealed that leadership from Saudi Arabia, Qatar, and the United Arab Emirates contacted Washington to request postponement of Tuesday’s scheduled operations. He indicated that “serious negotiations” are currently in progress with Tehran.

“I put it off for a little while, hopefully maybe forever, but possibly for a little while,” Trump stated during Monday evening remarks at the White House.

He emphasized that military action remains an option should diplomatic efforts fail to produce satisfactory results, though no specific timeframe was established.

Market participants seem to have already incorporated this volatility into pricing. Industry experts suggest Trump’s public statements are generating diminished market responses compared to earlier periods.

“These hot air verbal interventions from Trump used to have a heavy bearish impact on prices, but they now seem to have less and less effect unless they are backed by reality,” said Bjarne Schieldrop, chief commodities analyst at SEB AB.

Tehran has not yet publicly acknowledged that renewed diplomatic discussions are taking place.

Hormuz Blockade Continues Supporting Elevated Pricing

The Strait of Hormuz situation remains a focal point for energy traders. This critical shipping channel handles significant Persian Gulf petroleum exports, and its effective shutdown has constrained worldwide availability.

A US naval presence has rendered Iran’s Kharg Island export facility inoperative for a minimum of 10 days. This action has eliminated Tehran’s oil revenue stream while removing substantial volumes from international markets.

During the conflict’s initial phase, Iran prohibited other countries’ vessels from using the strait, positioning Tehran as the primary crude supplier through the passage during that period. This dynamic has since shifted.

Market observers indicate prices will likely maintain elevated levels until a concrete plan emerges for reopening the strategic waterway.

Oil benchmarks have climbed over 80% since January and advanced 20% during the past month, demonstrating the conflict’s significant impact on worldwide petroleum availability.

Moscow Crude Exemption Gets 30-Day Extension

In a separate development, Washington extended its sanctions exemption for Russian petroleum already loaded aboard vessels for another 30-day period.

Treasury Secretary Scott Bessent explained the extension aims to support stability in physical crude markets and guarantee supplies reach nations most “energy-vulnerable” to disruptions.

The prior exemption had expired only days before the replacement authorization was granted.

As of Tuesday’s close, petroleum prices maintain elevated positions with no definitive solution emerging for the Strait of Hormuz impasse.