Key Takeaways

- The S&P 500 has notched eight consecutive weeks of positive performance, with the Dow approaching the 51,000 milestone

- Major earnings releases scheduled from Dell, Marvell, Salesforce, Dollar Tree, Burlington, Gap, and Best Buy

- First quarter earnings expansion reaching 26% compared to last year, marking the strongest growth rate since 2021

- White House announces significant progress on Iran agreement focused on Strait of Hormuz access

- Technology sector companies positioning AI-related workforce reductions as strategic transformation initiatives

Equity markets enter May’s closing week maintaining strong momentum. With the S&P 500 trading near the 7,500 level, market participants are transitioning from earnings analysis to data interpretation and event monitoring.

Trading activity pauses Monday for the Memorial Day holiday, compressing market action into four sessions filled with corporate reports and economic releases.

Retail Sector Takes Spotlight

Multiple prominent retail chains will unveil their first-quarter financial performance throughout the week. Dollar Tree, Burlington Stores, Gap, and American Eagle Outfitters are scheduled to deliver results.

Market watchers are focused on consumer resilience among lower-income demographics facing headwinds from elevated fuel costs and inflationary pressures. Dollar store operators will face particular scrutiny regarding any evidence of spending pullback from their primary customer base.

Best Buy delivers its quarterly report Wednesday. This earnings presentation marks one of the initial appearances for newly appointed CEO Jason Bonfig, drawing significant investor attention.

The previous week delivered mixed signals from the retail landscape. Walmart provided conservative near-term projections while maintaining annual forecasts. Target surpassed analyst estimates and upgraded guidance. Nevertheless, both companies experienced share price declines.

Apparel retailers provided more encouraging results. VF Corp, Amer Sports, and Ralph Lauren each delivered robust performance, triggering stock appreciation.

Technology and AI Companies Return to Spotlight

Wednesday features financial results from Marvell Technology, which has surged 120% year-to-date. Salesforce also announces results that day, though the company has failed to capitalize on AI momentum with shares remaining more than 30% below year-ago levels.

Dell Technologies delivers earnings Thursday. Company leadership has previously characterized the AI opportunity as fundamentally transformative, and market participants will evaluate whether this optimism persists.

Synopsys completes the AI-connected reporting group, announcing results Wednesday following market close. The company’s shares received a lift when activist investor Elliott Investment Management revealed its position.

These announcements follow Nvidia’s previous week results, which demonstrated ongoing robust demand for AI infrastructure investment. Aggregate quarterly earnings expansion reached 26% year-over-year per Bank of America data, representing the most vigorous growth since 2021.

Bank of America analyst Savita Subramanian observed that despite management teams adopting measured language during earnings calls, forward guidance exceeded both average expectations and historical norms.

Iran Negotiations and Economic Indicators

President Trump announced Saturday that substantial progress had been achieved on an Iran agreement, with formal disclosure expected shortly. The framework reportedly addresses reopening the Strait of Hormuz, a critical global maritime passage that has experienced disruption since conflict erupted earlier this year.

Financial markets have previously responded to Iran-related developments, only to witness negotiations collapse. Secretary of State Marco Rubio has counseled restraint, emphasizing uncertainty until finalization.

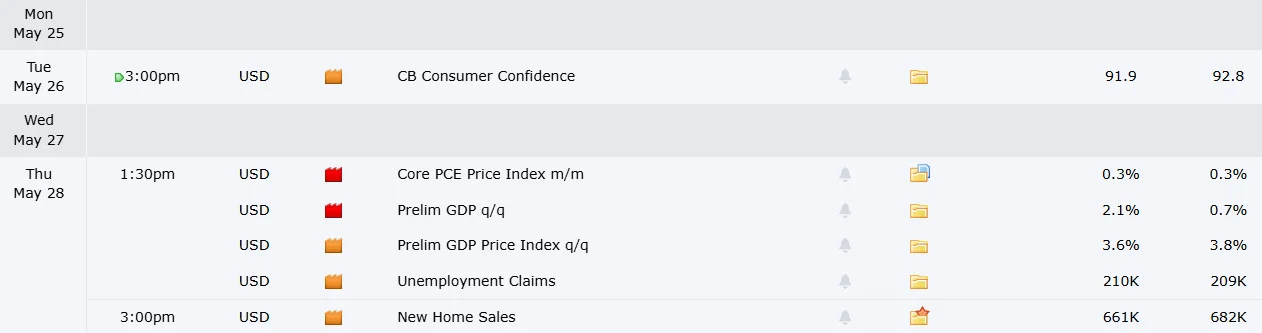

Regarding economic releases, the Conference Board publishes its Consumer Confidence Index on Tuesday. The Personal Consumption Expenditures index, representing the Federal Reserve’s favored inflation gauge, arrives Thursday.

Consumer sentiment weakened in the University of Michigan’s recent survey, yet Americans have maintained spending patterns despite negative sentiment readings — a disconnect that has persisted longer than many forecasters anticipated.

Technology sector workforce reductions continue generating headlines. Companies including Meta are characterizing employment cuts as AI-enabled strategic evolution rather than conventional cost containment. While overall layoff volumes remain modest, the pattern draws increased scrutiny as artificial intelligence adoption expands beyond technology sector pioneers.