Quick Summary

- Brent crude tumbled 6–7% to approximately $92 Tuesday following Monday’s spike above $119

- President Trump indicated the Iran conflict was progressing faster than his projected 4–5 week timeframe

- The IRGC dismissed Trump’s assessment and warned of potential regional oil export blockades

- G7 countries announced readiness to tap strategic petroleum reserves but have not yet acted

- Goldman Sachs maintains its $66/barrel Brent projection for Q4 2026 amid ongoing uncertainty

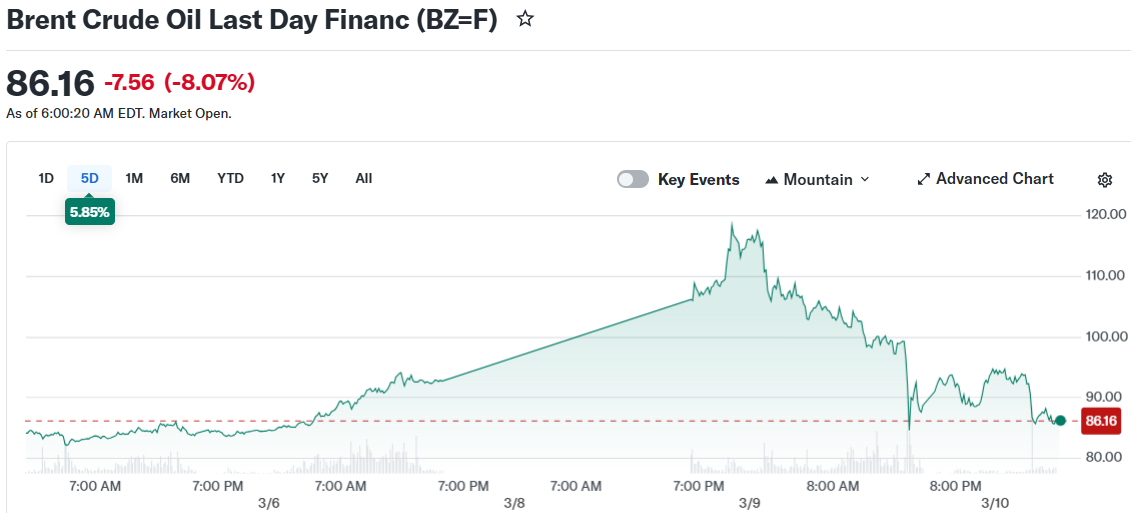

Energy markets experienced dramatic volatility this week as contradictory messages from Washington and Tehran created uncertainty among traders. Brent crude plummeted approximately 7% Tuesday, settling near $92 per barrel—a stark reversal from Monday’s climb above $100, marking the first time since mid-2022.

Monday’s rally stemmed from supply disruption concerns. With Saudi Arabia and allied producers implementing output reductions amid escalating U.S.-Israeli operations against Iran, Brent climbed to $119.50 while West Texas Intermediate reached $119.48. Dow Jones Market Data confirmed this represented the most significant single-day intraday movement ever recorded.

Markets reversed course following Trump’s CBS News interview Monday, where he characterized the conflict as “very complete” and noted operations were proceeding “very far ahead” of his original four-to-five week estimate. This statement alone triggered substantial selling pressure in crude markets.

A Monday conversation between Vladimir Putin and Trump, during which the Russian president presented rapid settlement proposals, further reinforced expectations of de-escalation and amplified the price decline.

However, not all parties agree the conflict is nearing conclusion.

Tehran Rejects U.S. Assessment

Tuesday brought strong pushback from Iran’s Islamic Revolutionary Guard Corps, which declared that they—not Washington—would “determine the end of the war.” The military organization further warned it would halt all regional oil shipments if U.S. and Israeli military operations persist.

In a separate PBS News interview covered by the Wall Street Journal, Iranian Foreign Minister Abbas Araghchi categorically rejected any diplomatic engagement with Washington.

Trump fired back via Truth Social, cautioning Iran that any attempt to obstruct the Strait of Hormuz would provoke a U.S. response “twenty times harder than they have been hit thus far.”

Market observers suggest investors may be overreacting. “While there was an overreaction to the upside yesterday, we think there is an overreaction to the downside today,” observed Suvro Sarkar, DBS Bank’s energy sector team lead.

Sarkar highlighted that Murban and Dubai oil grades continued trading above $100 per barrel, indicating physical market fundamentals remained relatively unchanged.

Government Response Measures

G7 finance ministers convened Monday to evaluate strategic petroleum reserve releases. While they declined immediate action, their joint statement affirmed they “stand ready to take necessary measures,” explicitly including potential stockpile deployments.

Reports indicate Trump is exploring Russian oil sanctions relief as part of comprehensive price stabilization efforts. Multiple sources have confirmed this policy option remains under active consideration.

Phillip Nova analyst Priyanka Sachdeva noted these combined developments—potential Russian sanctions adjustments, G7 reserve preparedness, and Trump’s optimistic remarks—provided sufficient justification for traders to exit panic-driven positions.

Goldman Sachs maintained its existing price outlook, keeping Brent projections at $66 per barrel and WTI at $62 per barrel for Q4 2026, emphasizing the situation’s evolving nature.

Tuesday’s IRGC declaration stands as the most recent concrete indication that hostilities continue unresolved.