Key Highlights

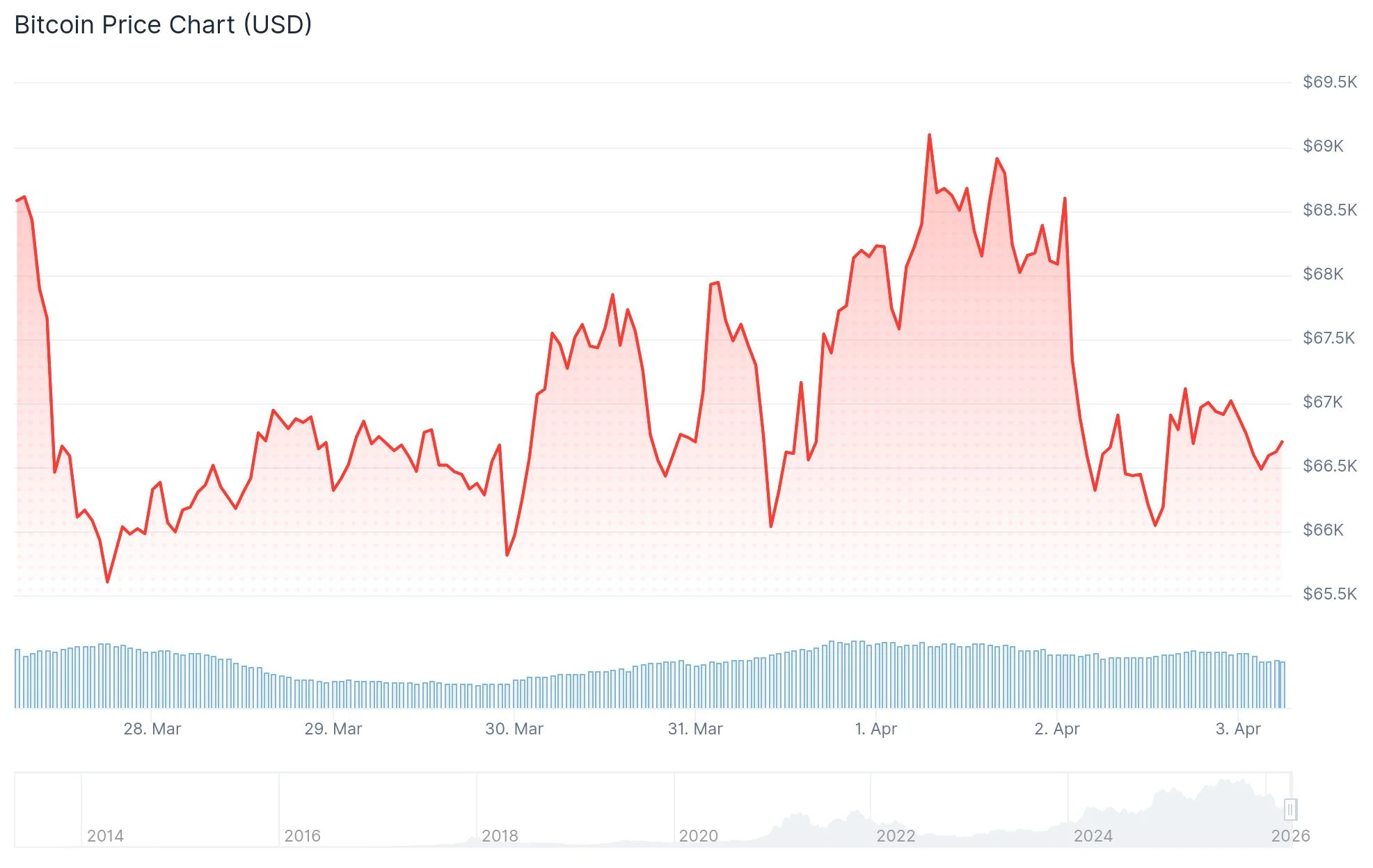

- BTC hovers near $66,600 as Easter weekend halts CME futures and ETF trading activity

- Net Bitcoin demand dropped to -63,000 BTC despite ETF inflows and corporate buying reaching their strongest levels in months

- Whale addresses holding 1,000–10,000 BTC have become net distributors, reducing holdings by approximately 188,000 BTC from cycle highs

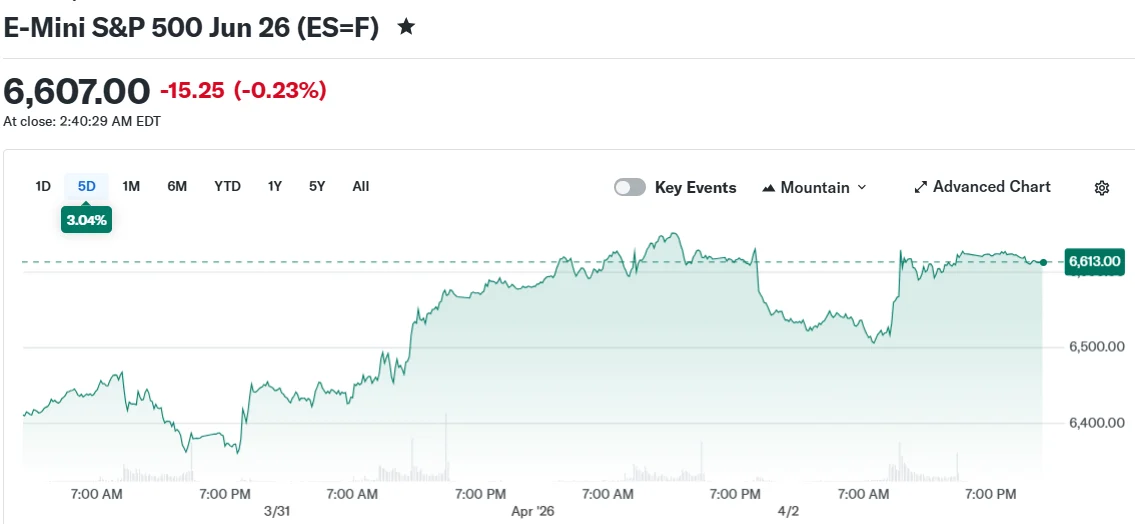

- Major U.S. equity indices broke their five-week decline, posting modest weekly gains

- WTI crude oil jumped 11% to $111.54, marking the biggest single-day dollar increase in over four decades

As the Easter holiday weekend approaches, Bitcoin faces headwinds while traditional equity markets managed to stage a modest recovery from recent losses.

BTC was changing hands around $66,600 on Thursday as Good Friday market closures shuttered CME futures and ETF trading platforms. This temporary halt eliminates two crucial demand channels precisely when purchasing momentum has already weakened.

According to CryptoQuant analytics, the 30-day apparent demand metric currently registers approximately -63,000 BTC. This negative reading persists despite ETF acquisitions reaching roughly 50,000 BTC during the past month—the strongest performance since October 2025.

Corporate treasury buyer Strategy accumulated approximately 44,000 BTC during this same timeframe. However, selling activity from other participants proved substantial enough to offset these significant inflows.

Whale Wallets Shift to Distribution Mode

The most evident indication of selling pressure emerges from large-balance addresses. Wallets containing between 1,000 and 10,000 BTC have transitioned into net distribution patterns. Their annual balance adjustment has declined to approximately -188,000 BTC, a dramatic reversal from the positive 200,000 BTC recorded during the 2024 market peak.

Medium-sized holders have similarly decelerated their accumulation activity. The Coinbase Premium indicator has maintained negative territory, traditionally signaling diminished appetite from institutional U.S. buyers.

Singapore-based liquidity provider Enflux explained to CoinDesk that Bitcoin’s downside support level remains partially anchored to Federal Reserve monetary policy expectations. This fundamental support structure now faces scrutiny.

The ISM manufacturing prices-paid component surged to 78.3 in March, reaching its highest point since June 2022. Such elevated readings diminish prospects for imminent rate reductions, consequently challenging Bitcoin’s macroeconomic price foundation.

ETF activity patterns already demonstrate this transition. The week ending March 24 recorded $296 million in net outflows from spot Bitcoin ETFs. Early April has witnessed subdued inflow levels.

CryptoQuant analysts identified a technical resistance band spanning $71,500 to $81,200 for any potential upside recovery. The upcoming critical data release is the U.S. core PCE inflation report scheduled for April 9.

Equity Markets and Energy Commodities

U.S. stock indices finished the week with gains despite Thursday’s pullback. The Dow Jones Industrial Average declined 61 points during Thursday’s session, yet all three primary benchmarks secured positive weekly performance, breaking a five-week losing sequence.

The trading day was characterized by extraordinary movement in energy markets. West Texas Intermediate crude closed at $111.54 per barrel, advancing 11% during the session. The $11.42 dollar increase represents the largest single-session advance in WTI records extending back to 1983.

The dramatic surge followed President Trump’s address regarding Iranian tensions, which provided no concrete developments toward resolving the Strait of Hormuz blockade situation.

J.P. Morgan strategist Fabio Bassi projected that crude prices will maintain elevated levels throughout the second quarter. He positioned near-term risk in the $120–$130 per barrel territory, with scenarios above $150 becoming plausible if Strait disruptions extend into mid-May.

Market participants will also monitor the March employment situation report, scheduled for Friday release despite equity market holiday closures. Analysts anticipate a hiring rebound following February’s weather-disrupted and strike-impacted results.