TLDR

- The greenback trades near annual peaks amid growing Federal Reserve tightening expectations

- Real yields on 10-year Treasuries surged past 2.3%, marking the highest point in more than 12 months

- Military confrontations between the U.S. and Iran resulted in closure of the Strait of Hormuz

- Crude oil jumped 2%, with Brent trading at $77.60, intensifying inflationary pressures

- Sterling dipped 0.1% versus the dollar; the euro has depreciated 2.7% year-to-date in 2026

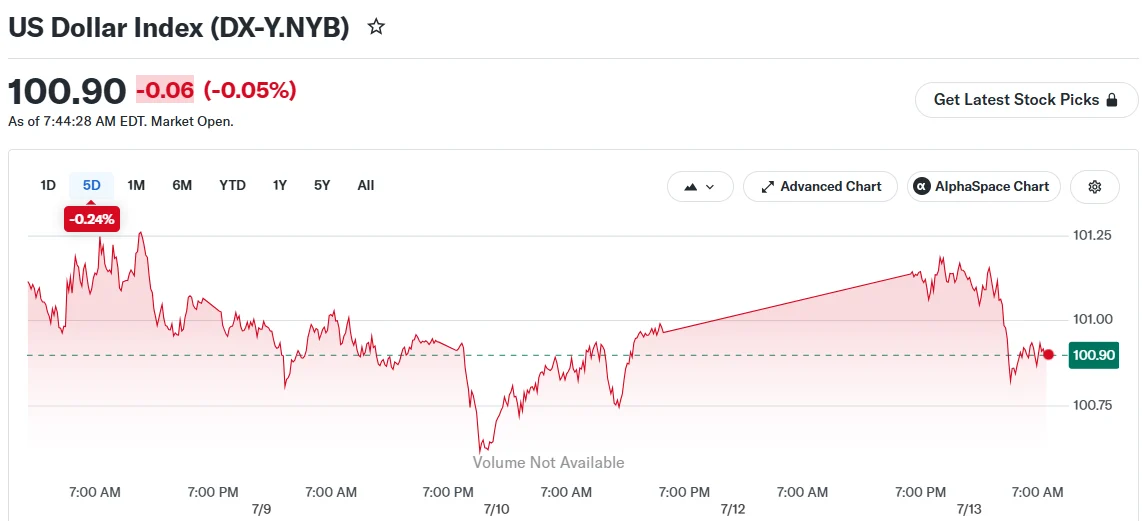

The American currency continues trading close to its strongest position of 2026, propelled by a mix of robust economic indicators, mounting inflation anxieties, and fresh military tensions involving the United States and Iran.

Market participants anticipate the Federal Reserve will maintain elevated interest rates — or potentially implement additional increases. Current money market pricing suggests approximately 37 to 40 basis points of monetary tightening by year’s conclusion, representing a significant shift from early June forecasts.

The Bloomberg Dollar Spot Index remains anchored near 2026 peaks. Speculative positioning reveals the most aggressive bullish dollar stance since 2015, with net long exposure exceeding $40 billion across currency futures.

Inflation-Adjusted Treasury Returns Hit 12-Month Peak

The 10-year real Treasury yield — which strips out inflation expectations — recently crossed above 2.3%. This represents the loftiest level witnessed in over a year, reflecting market conviction that restrictive monetary policy will persist.

Elevated real yields enhance the appeal of dollar-based investments for international capital. However, they simultaneously depress bond valuations, creating challenges for holders of extended-duration U.S. sovereign debt.

Portfolio managers are adapting strategies by embracing dollar strength while reducing exposure to longer-maturity Treasuries. Numerous institutional investors are financing dollar-long positions through short positions in lower-yielding alternatives such as the euro and Japanese yen.

Multiple major financial institutions, Bank of America among them, project sustained elevation in real yields alongside continued Fed hawkishness, especially relative to currencies from dovish central banks.

Dissenting views exist, however. Certain market observers contend that employment data shows softening and that real yields may have approached their cyclical zenith. These analysts suggest the appreciating dollar combined with rising yields already constitute tightening financial conditions, potentially diminishing the necessity for additional Fed intervention.

Middle East Hostilities Amplify Energy and Currency Volatility

Throughout the weekend extending into Monday, American and Iranian military forces conducted reciprocal missile and unmanned aerial vehicle operations. Tehran targeted U.S. installations across the region while announcing renewed closure of the Strait of Hormuz, a critical artery for international petroleum transport.

Pentagon officials confirmed retaliatory strikes against Iranian air defense infrastructure and coastal surveillance installations.

Brent crude oil advanced 2% to reach $77.60 per barrel. Escalating energy costs compound inflation concerns, thereby reinforcing arguments favoring additional Federal Reserve rate increases.

The British pound retreated 0.1% to $1.339 during Monday trading. Year-to-date, sterling has depreciated 0.6% against the dollar. The euro has weakened 2.7% versus the greenback during the comparable timeframe.

Lee Hardman, senior currency strategist at MUFG, characterized the foreign exchange reaction as “relatively modest so far,” while cautioning that substantially higher petroleum prices could emerge as a more powerful driver of dollar appreciation.

Federal Reserve Chairman Kevin Warsh faces congressional testimony this week, coinciding with fresh U.S. inflation data releases. Either development carries potential to materially reshape interest rate expectations.