Key Takeaways

- Weekend military exchanges between US and Iran triggered market volatility

- Nasdaq 100 futures declined 1%, S&P 500 futures slipped 0.3%

- Brent crude surged 3.8% toward $79 amid Strait of Hormuz concerns

- Bitcoin declined 1.6% to $62,943 as risk appetite diminished

- Critical inflation reports and major bank earnings scheduled this week

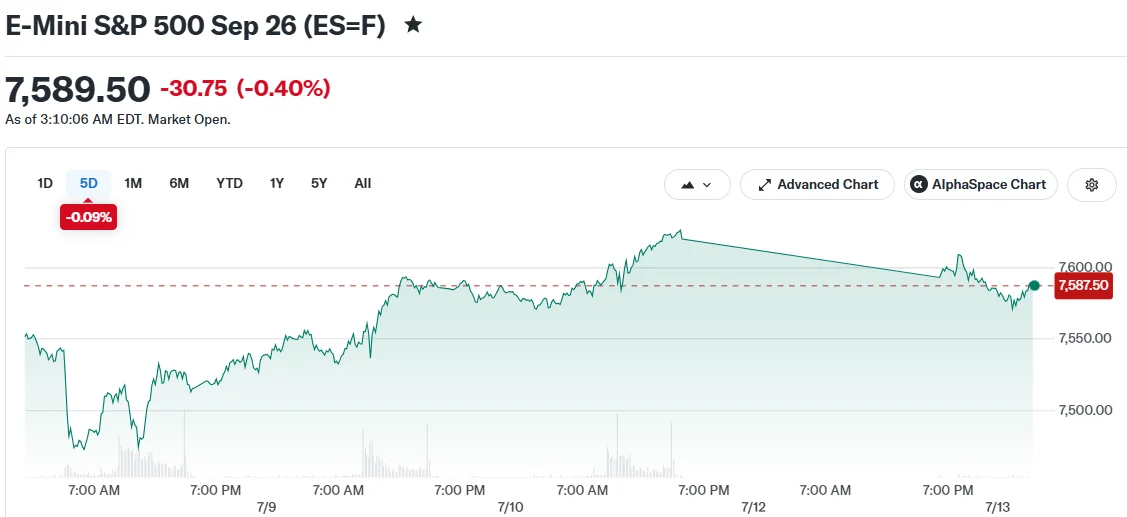

Equity futures declined during Monday’s pre-market session following weekend military actions between the United States and Iran. Nasdaq 100 futures registered a 1% decline, S&P 500 futures dropped 0.3%, while Dow Jones futures remained relatively unchanged.

The renewed Middle Eastern conflict unnerved market participants who have been monitoring regional tensions with increasing concern. Despite both the S&P 500 and Nasdaq recording modest weekly advances, those gains now face significant pressure.

Iran’s Islamic Revolutionary Guard Corps announced the Strait of Hormuz would be “closed until further notice.” American officials contradicted this claim, maintaining the waterway remains operational. Shipping data from tracking company Kpler indicates no LNG vessels have passed through the strait since Saturday.

Oil prices experienced substantial increases following these developments. Brent crude advanced 3.8% to reach $78.89 per barrel. West Texas Intermediate gained 3.7% to $74.04 per barrel. Deutsche Bank’s Jim Reid noted that oil markets had “reacted” to reports of vessel damage, intercepted drone activity, and strikes on energy-related infrastructure throughout the Gulf region.

President Trump indicated ceasefire negotiations with Iran continue, while simultaneously declaring he views the existing ceasefire as “over.” This conflicting messaging has heightened investor uncertainty.

Critical Economic Data and Corporate Earnings Ahead

The geopolitical escalation arrives during a crucial period for financial markets. Two significant inflation indicators are scheduled for release this week. The Consumer Price Index publishes Tuesday, with the Producer Price Index following on Wednesday.

These economic reports will provide investors insight into whether Middle Eastern developments are contributing to wider inflationary pressures. The data will also influence expectations regarding Federal Reserve monetary policy decisions in coming months.

Corporate earnings season commences in full force this week. JPMorgan Chase, Goldman Sachs and Bank of America headline Tuesday’s bank reporting schedule. Netflix and UnitedHealth will also release quarterly results.

Taiwan Semiconductor Manufacturing Company announces earnings this week as well. Its performance is anticipated to offer valuable perspective on artificial intelligence chip demand, a topic commanding significant Wall Street attention.

The artificial intelligence investment theme has experienced weakening momentum recently. Market participants are questioning the sustainability of substantial AI infrastructure expenditures by major technology corporations.

South Korean memory chip manufacturer SK Hynix experienced a 15% share price decline Monday following its Friday debut on US exchanges. The selloff contributed to a 9% drop in South Korea’s KOSPI index, underscoring persistent doubts about the AI investment cycle’s longevity.

Cryptocurrency Retreats Amid Risk-Off Sentiment

Bitcoin decreased 1.6% during the past 24 hours to $62,943. The decline mirrors a wider retreat from risk-oriented assets as geopolitical tensions intensified.

The 10-year US Treasury yield increased 1 basis point to 4.57%. The US dollar index weakened 0.1% versus a basket of major currencies.

With petroleum prices surging, inflation metrics approaching, and earnings season launching, this week is positioned to become among the most consequential trading periods of the year for market participants.