Key Takeaways

- Military action against Iran by the U.S. created immediate market turbulence, with crude oil climbing and equities declining at Monday’s open

- Major indexes including the S&P 500 and Nasdaq reversed losses and traded in positive territory by Monday afternoon

- Leading financial strategists recommend investors capitalize on market weakness

- Market analysis reveals stocks posted gains 12 months following four of five comparable geopolitical events since 1990

- Federal Reserve interest rate reductions could provide additional market tailwinds if tensions persist

Weekend military operations by the United States targeting Iran created immediate turmoil across global financial markets when trading commenced Monday. Crude oil prices surged, equity markets retreated, and government bond yields moved higher as market participants digested the developing situation.

However, the selloff proved short-lived. Both the S&P 500 and Nasdaq Composite reversed course and entered positive territory by Monday afternoon. The Dow Jones Industrial Average similarly recovered substantially from its early session lows.

Nvidia advanced 2.9% during Monday’s session. Apple added 0.2%, contributing to a 0.4% increase in the broader Magnificent Seven technology index.

The iShares Expanded Tech-Software Sector ETF had declined approximately 35% from its September high point. The fund has subsequently rebounded over 7.6% from the prior week’s bottom.

A research note from JPMorgan analyst Mislav Matejka advised investors with extended investment horizons “should be using the weakness” as an opportunity to increase allocation to risk assets. His assessment emphasized that underlying fundamentals continue to look favorable.

BTIG’s chief market technician Jonathan Krinsky used the headline “When Missiles Fly, Time to Buy” for his analysis. He characterized the market movement as a tactical buying opportunity rather than a signal to exit positions.

Adrian Helfert from Westwood highlighted that maintaining market exposure has proven correct following every similar geopolitical incident since 1990. Examining five comparable crisis events, equity markets posted positive returns 12 months later in 80% of instances.

Historical Performance Following Geopolitical Crises

Ryan Detrick from Carson Group references historical information indicating the S&P 500’s median advance three months following significant market disruptions stands at 2.7%. Extending to 12 months, returns climb to 7.4%, with positive performance occurring 65% of the time.

Following the Hamas attack on Israel dated October 7, 2023, international equities posted gains throughout the subsequent year. When the Iraq War commenced in 2003, stocks climbed nearly 30% over the following 12 months.

Veteran market strategist Ed Yardeni anticipates any elevation in oil prices will prove transient. His view suggests reduced gasoline costs could enhance consumer spending capacity and drive inflation nearer to the Federal Reserve’s 2% objective.

Tigress Financial Intelligence’s Ivan Feinseth indicated the Federal Reserve might consider rate reductions should the conflict extend over time. Rate reduction timing could accelerate if Kevin Warsh receives confirmation as Jerome Powell’s replacement for Fed chair.

Critical Support Levels for the S&P 500

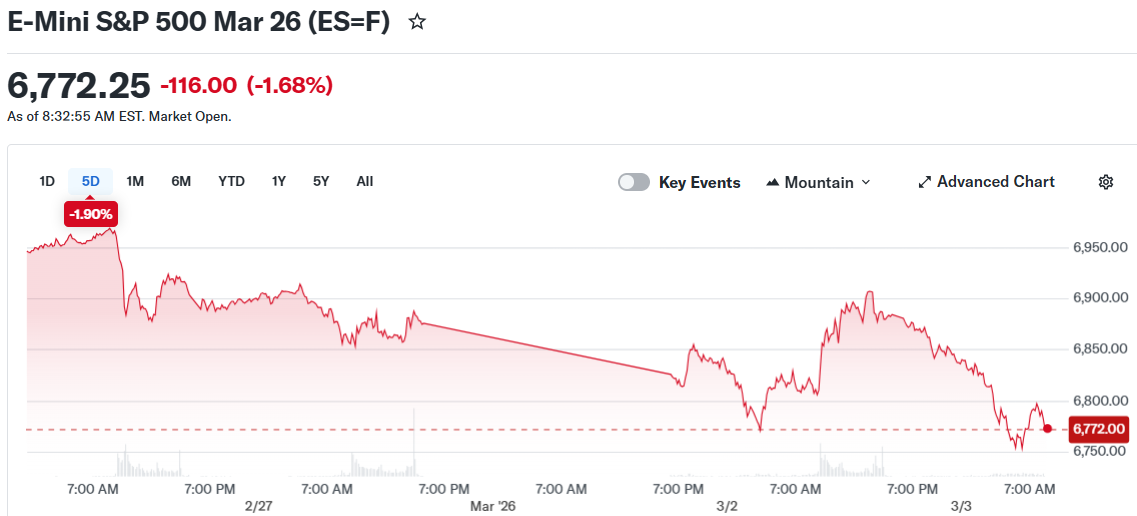

Futures contracts pointed to losses Tuesday morning, with Dow futures declining nearly 800 points. Brent crude was changing hands above $83 per barrel.

The VIX volatility index held above 20, a threshold typically interpreted as indicating heightened investor apprehension. The S&P 500 has posted a modest 0.5% gain year-to-date.

Adam Turnquist from LPL Financial cautioned that a decline through 6,775 points on the S&P 500 could prompt retesting of November’s low at 6,522. Technical analysts are monitoring this threshold with particular attention.