Key Takeaways

- The U.S. dollar maintained strength near 12-month highs following increased market expectations for Federal Reserve rate increases

- Japan’s yen declined toward 161.73 per dollar, approaching its weakest position since the mid-1980s

- Political upheaval in Britain following Prime Minister Keir Starmer’s resignation announcement pressured sterling downward

- Diplomatic progress between Washington and Tehran on a potential agreement within two months drove crude oil prices down approximately 2%

- Market positioning data reveals speculators hold their most bullish dollar stance in over a year, totaling roughly $30 billion

The U.S. dollar continues trading near its most robust position in twelve months as financial markets anticipate the Federal Reserve will implement interest rate increases. Meanwhile, Japan’s currency hovers dangerously close to a four-decade nadir, and political developments in the United Kingdom triggered sterling’s decline.

Following last week’s Federal Reserve policy meeting, officials indicated the possibility of rate adjustments before year-end. This communication prompted market participants to accelerate their timeline for monetary tightening.

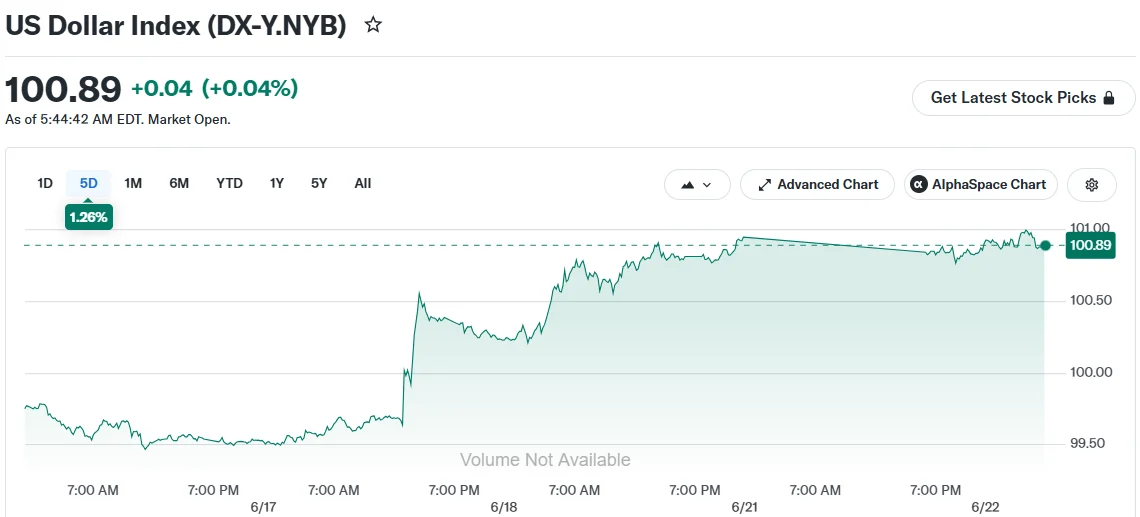

The dollar index—a benchmark measuring the greenback’s performance against a basket of six major global currencies—was positioned around the 101 level. This represents nearly a 3% appreciation since the beginning of the calendar year.

Speculative traders have significantly increased their bullish dollar positions. According to Commodity Futures Trading Commission records, these wagers have reached approximately $30 billion—marking the highest level witnessed in sixteen months.

Jeremy Stretch, who leads G10 currency strategy at CIBC, indicated the dollar should maintain its firmness. He emphasized that continued market pricing for at least one Fed rate increase this year provides additional upside potential for the greenback.

Stretch further suggested that even potential action from the Bank of Japan to raise rates might prove insufficient to reverse the dollar’s advance against the yen.

Japanese Currency Approaches Multi-Decade Weakness

The Japanese yen was exchanging hands at approximately 161.73 against the dollar during Monday trading. A breach above 161.96 would mark the currency’s weakest reading since the Reagan administration era.

Japan’s Finance Minister Satsuki Katayama stated that government officials stand prepared to address foreign exchange movements whenever necessary.

However, market observers express doubt about intervention effectiveness. Matt Simpson, a senior market analyst at StoneX, suggested Tokyo authorities may perceive themselves as “powerless” against the substantial momentum generated by Federal Reserve rate expectations.

Japanese authorities deployed a historic 11.7 trillion yen in market intervention efforts as recently as late April. Those temporary gains have subsequently evaporated completely.

British Political Turmoil Pressures Sterling

UK Prime Minister Keir Starmer announced his intention to step down on Monday, triggering a 0.1% decline in the pound to $1.322.

Andy Burnham, a Labour Party rival, emerges as the leading candidate for succession. Burnham has communicated to financial markets his intention to maintain adherence to Britain’s fiscal framework.

Lee Hardman, an analyst with MUFG, observed that this pledge has offered some market comfort, helping to contain sterling’s downside pressure for the time being.

Crude Prices Retreat Following Diplomatic Breakthrough

Negotiations between Washington and Tehran yielded a framework for achieving a comprehensive agreement within a 60-day timeframe, according to statements from mediating countries Qatar and Pakistan. Oil prices retreated nearly 2% following the announcement, with Brent crude settling at $79.10 per barrel.

Iran simultaneously declared it had restricted access through the Strait of Hormuz, maintaining some degree of market uncertainty.

Thu Lan Nguyen, an analyst at Commerzbank, observed that declining oil prices have not undermined dollar strength because interest rate expectations remain the dominant driver. Should petroleum prices rebound and intensify inflationary pressures, that development could further strengthen rate increase expectations—and consequently boost the dollar even more.

The dollar index achieved a one-year pinnacle of 101.127 on Friday before experiencing a modest retreat during Monday’s session.