TLDR

- The greenback declined following Trump’s announcement that an Iran agreement may be reached within days

- Crude oil tumbled to eight-week lows amid expectations of reduced tensions and stabilized energy flows

- The European currency reached a weekly peak, heading toward its strongest weekly performance in over 30 days

- May producer price data exceeded expectations while underlying inflation measures fell short of projections

- The central bank is anticipated to maintain current rates next week; traders see 60% probability of December increase

The American dollar weakened Friday following President Donald Trump’s statement that an agreement with Iran might be completed within the coming days. Trump indicated that Iran’s Supreme Leader had approved the framework, reducing concerns about additional military confrontation in the region.

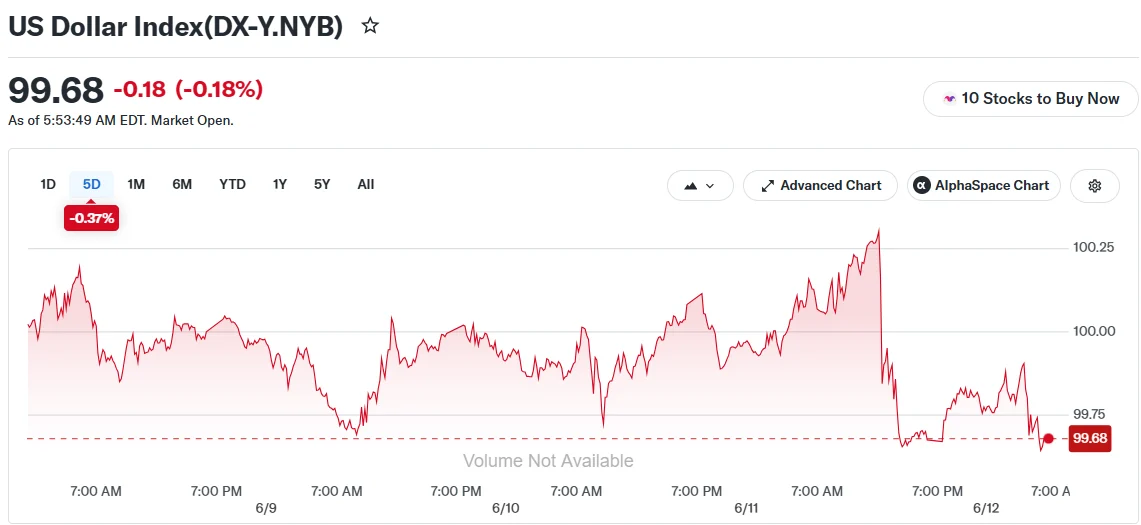

The U.S. Dollar Index declined 0.1% to 99.803 during London trading hours, reaching a weekly low in overnight sessions. The index was trending toward a 0.3% loss for the week.

When market confidence strengthens, the dollar typically weakens. This occurs as traders shift capital away from defensive positions when concerns about worldwide instability diminish.

“Currently, markets are experiencing relief that additional tensions might be prevented, and progress toward an agreement appears promising,” said Jefferies economist Mohit Kumar.

Oil prices experienced significant declines as well, reaching approximately two-month lows. The drop in energy costs created additional downward momentum for the dollar, considering America’s position as a net petroleum exporter.

European Currencies Maintain Strength

The euro remained close to its weekly high and was positioned for its most substantial weekly advance in more than 30 days. The European Central Bank’s initial rate boost in nearly three years provided currency support.

Britain’s currency showed minimal movement Friday while maintaining its trajectory for the strongest weekly showing in almost a month. The pound disregarded figures indicating the U.K. economy shrank 0.1% during April, marking the first monthly contraction since August.

The pound’s recent momentum remains vulnerable. Market participants are monitoring the June 18 Makerfield by-election intensely, as outcomes could carry political implications for Prime Minister Keir Starmer.

The Bank of England convenes next week with widespread anticipation of maintaining current rates. Officials confront challenges from both persistent inflation and economic deceleration.

“Elevated costs connected to Middle East tensions are anticipated to maintain pressure on a vulnerable UK economy,” said Danni Hewson of AJ Bell.

Federal Reserve Under Scrutiny as Price Data Shows Divergent Trends

May’s U.S. producer price index climbed beyond projections, primarily attributed to elevated energy expenses linked to previous Middle East instabilities. Nevertheless, core producer prices, excluding volatile food and energy components, increased less than anticipated.

The divergent figures reduced some concerns regarding an immediate Federal Reserve rate adjustment. Markets shifted expectations for additional tightening measures toward year-end.

The Fed convenes next week with broad expectations of maintaining current policy. Traders will scrutinize Chair Jerome Powell’s remarks carefully for guidance on future direction.

Markets currently indicate approximately a 60% probability of a rate boost by December, based on CME FedWatch data.