Key Takeaways

- Long-term Treasury yields have climbed sharply following the outbreak of conflict between the U.S. and Iran in late February, with the 30-year bond reaching its highest point in nearly two decades.

- Consumer price inflation accelerated to 3.8% in April, with projections suggesting it could surge to 6.7% by the second quarter as energy costs ripple through the economy.

- Market expectations have completely reversed course — instead of anticipated rate cuts, traders now see the Federal Reserve hiking rates as soon as early 2027.

- Historical data reveals that the S&P 500 has declined following each of the four Fed rate-hike cycles since 1999, with an average pullback of 7%.

- Equity markets rallied on diplomatic developments between Washington and Tehran, yet bond traders remained skeptical with critical economic data looming.

Geopolitical conflict between the United States and Iran has triggered a cascade of economic consequences: accelerating inflation, surging bond yields, and a dramatic shift in Federal Reserve policy expectations. Here’s a breakdown of these developments and their implications for market participants.

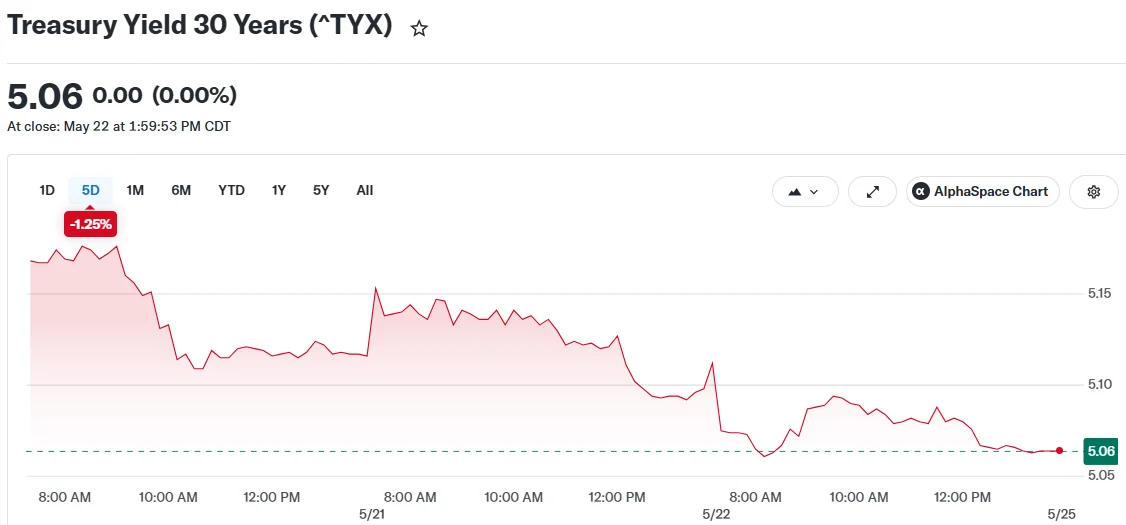

Bond Yields Reach Multi-Year Peaks

The conflict that erupted in late February immediately impacted global energy markets. Iran’s closure of the Strait of Hormuz — a critical conduit for international oil shipments — sent crude prices soaring. This energy shock has reverberated throughout the broader economy, driving up costs across multiple sectors.

The April consumer price index registered 3.8%, marking the highest inflation reading since 2023. Economists at the Federal Reserve Bank of Cleveland are forecasting inflation could climb as high as 6.7% during the current quarter’s latter half.

This inflationary pressure has prompted investors to dump Treasury securities. As bond prices decline, yields move inversely upward. The 2-year Treasury yield has jumped 75 basis points since hostilities commenced. Meanwhile, the 30-year bond is now offering over 5% — a level unseen in 19 years.

At the beginning of this year, market participants anticipated at least two Fed rate reductions. Current pricing from CME Group’s FedWatch tool indicates the central bank’s next policy adjustment will be an increase, potentially arriving by January 2027.

Historical Pattern Shows Stocks Struggle During Tightening Cycles

Elevated interest rates increase capital costs for corporations, potentially dampening investment activity and compressing profit margins. They also suppress consumer demand for expensive purchases that typically require financing.

Looking at the Fed’s four tightening cycles since 1999, the S&P 500 experienced losses in every instance during the subsequent three-month period. The mean decline registered 7%, with drawdowns spanning from 1% to 17%.

Despite these headwinds, the S&P 500 has advanced approximately 9% year-to-date, buoyed by robust corporate earnings. However, some market observers caution that this strength may be concealing underlying vulnerabilities.

“The S&P 500 is still riding a wave of euphoria from a blowout earnings season, but with that over for the next couple of months, the likelihood of a summer selloff is high,” said Dennis Follmer, chief investment officer at Montis Financial.

Diplomatic Progress Boosts Equities While Bonds Remain Unconvinced

Tuesday’s trading session saw equity indices surge on news that peace negotiations between Washington and Tehran were approaching completion. The Nasdaq jumped approximately 300 points, driven by technology heavyweights including Nvidia, Intel, and Micron Technology. The S&P 500 opened nearly 50 points higher.

Crude oil markets experienced volatile movements. Brent crude spiked more than 3% to reach $96.43 per barrel during early trading, though prices remain roughly 8.6% beneath Friday’s closing level.

Secretary of State Marco Rubio characterized the negotiations as entering their concluding phase while noting they might require “a few more days” to finalize. Simultaneously, Iran’s Revolutionary Guard reported engaging a U.S. aircraft that allegedly violated Iranian airspace, creating uncertainty around the diplomatic timeline.

Fixed-income markets displayed considerably less enthusiasm. The 10-year Treasury yield maintained its position above 4.5%. The 30-year bond continued trading above 5%. Investors are exercising caution before Thursday’s release of April inflation metrics and first-quarter GDP data.

“Bond markets are sending a pretty strong signal that they see choppier waters ahead,” Follmer added.

Paul Donovan, global chief economist at UBS Wealth Management, acknowledged progress in talks but said “a deal still seems some way off.”

This week’s economic calendar includes new residential sales data and weekly unemployment claims figures, alongside Thursday’s inflation and GDP releases. These indicators will likely determine market sentiment heading into the weekend.