Stock Earnings Preview: What Investors Should Watch This Week")

Quick Overview

- Nvidia’s first-quarter results arrive Wednesday, with Wall Street projecting $1.78 earnings per share and $79.2 billion revenue

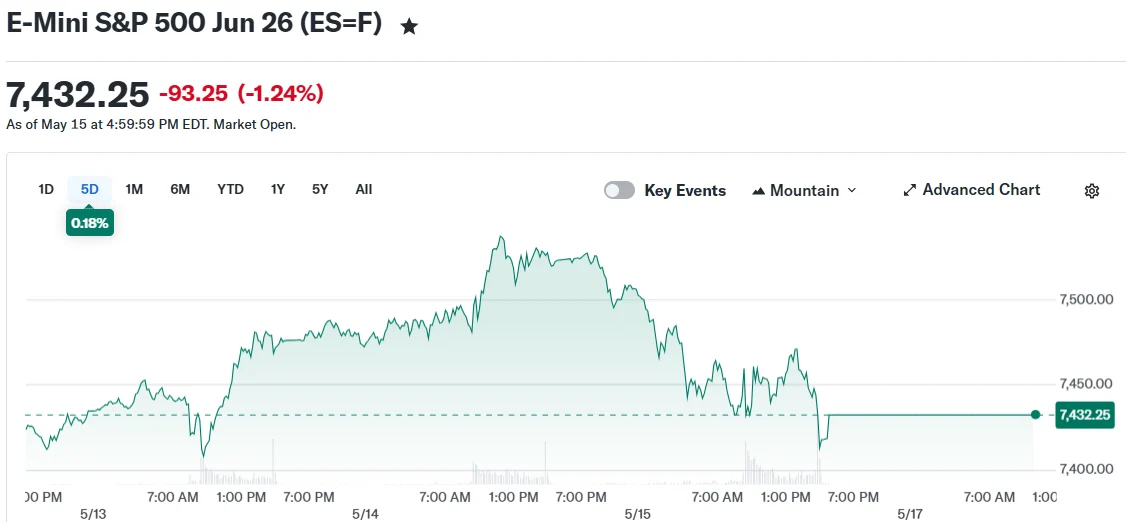

- The S&P 500 fell 1.2% Friday, wrapping up seven consecutive weekly advances on a downbeat note

- Treasury yields on the 10-year note surged beyond 4.5%, maintaining market headwinds

- Carlyle Group’s Jeff Currie suggests commodities could be launching into a prolonged bull market

- Walmart’s Thursday earnings will spotlight inflation trends and spending patterns following April’s 3.8% CPI reading

Market participants enter the trading week grappling with multiple challenges. Friday brought equity declines, Treasury yield increases, and lingering uncertainty from recent Trump-Xi diplomatic meetings.

The S&P 500 surrendered 1.2% Friday, though it eked out a 0.1% weekly advance — marking its seventh consecutive weekly rise. The Nasdaq tumbled 1.5% Friday, closing the week marginally lower at roughly negative 0.1%. The Dow Jones also finished the week in red territory, declining 0.2%.

The 10-year Treasury yield decisively broke above 4.5% Friday, a threshold that typically triggers caution among stock market participants. This benchmark figure will remain a critical focus point as trading resumes.

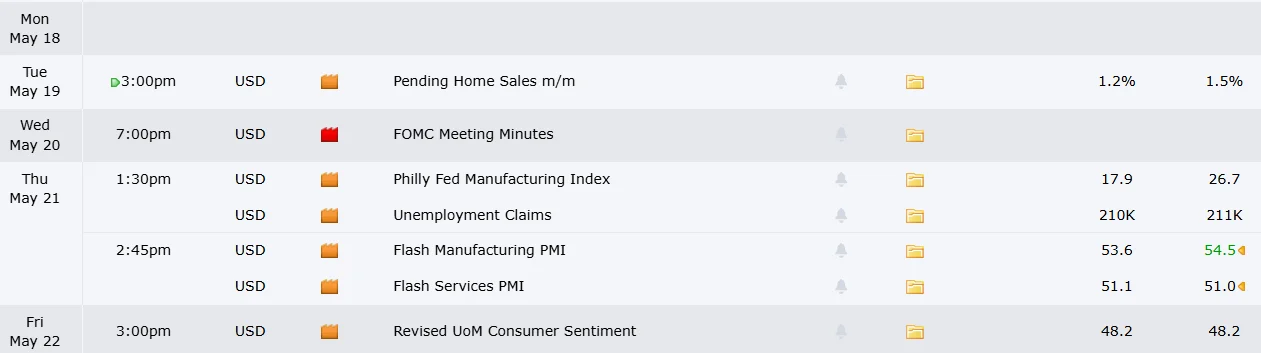

While the economic calendar appears less crowded than previous weeks, one corporate event dominates investor attention.

Nvidia’s Quarterly Report Commands Spotlight

Nvidia will unveil its first-quarter financial performance Wednesday following market close. The semiconductor giant holds the distinction of being the world’s most valuable corporation, having surpassed $5.7 trillion in market capitalization last week.

Wall Street consensus calls for adjusted earnings of $1.78 per share alongside revenue reaching $79.2 billion.

Back in March, Nvidia’s CEO Jensen Huang characterized demand for the company’s products as extraordinarily strong. He expanded forecasts for two major product categories, projecting they could generate over $1 trillion by late 2026.

Huang recently accompanied President Trump on a diplomatic mission to China, engaging with government representatives and corporate executives. Market watchers will scrutinize any discussion regarding potential agreements or transactions stemming from that visit.

Reporting from Reuters last week indicated that major Chinese technology firms such as Alibaba, Tencent, ByteDance, and JD.com received authorization to purchase Nvidia’s H200 processors. This development propelled shares to record territory Thursday before Friday’s retreat.

Despite the impressive rally, UBS analyst Tim Arcuri observed that many institutional investors maintain subdued expectations entering the announcement, potentially creating conditions for a favorable market response if results exceed forecasts.

Bank of America analyst Vivek Arya highlighted that market participants will also seek insights regarding competitive threats from Advanced Micro Devices, Broadcom, and emerging player Cerebrus, which completed its initial public offering last week.

Walmart, Retail Sector, and Consumer Health

Walmart delivers its quarterly results Thursday morning. Investor attention will be heightened given that April’s Consumer Price Index registered a 3.8% year-over-year increase, primarily fueled by energy price escalation.

During the previous quarter, Walmart characterized its customer base as “resilient.” This week’s report will test whether that assessment remains accurate.

Target also announces results Wednesday. Newly appointed CEO Michael Fiddelke has presented strategies aimed at restoring company expansion. Home Depot and Lowe’s release earnings Tuesday and Wednesday respectively, though both face challenges amid sluggish housing market conditions.

The University of Michigan’s consumer sentiment survey and inflation expectations data arrive Friday, completing the week’s economic landscape.

Is a Commodity Supercycle Beginning?

Carlyle Group energy strategist Jeff Currie published an extensive analysis Friday suggesting markets may be witnessing the early stages of an extended commodity bull market.

Currie highlighted AI’s escalating requirements for tangible infrastructure — including energy resources, industrial metals, and computing hardware — as a primary catalyst. He also referenced the Iran situation, which Goldman Sachs estimates has eliminated more than 13.7 million barrels daily from global oil markets, representing the largest energy supply disruption in recorded history.

Currie maintains that investment capital has concentrated heavily on the AI trade while the physical commodities essential for AI operations have suffered from chronic underinvestment. He contends this structural mismatch is now beginning to self-correct.