Key Takeaways

- Major indexes posted fresh all-time highs last week, powered by semiconductor and artificial intelligence momentum

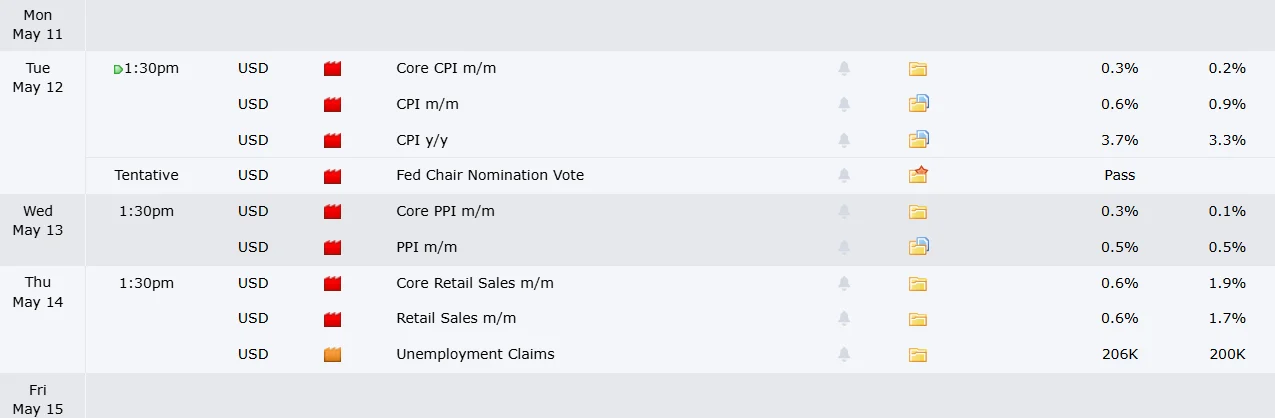

- Tuesday brings April inflation figures; focus centers on energy costs following March’s 20%+ surge

- Semiconductor sector soared, with Micron climbing nearly 38% weekly and Intel rallying on potential Apple partnership

- Major quarterly reports arrive from Cisco, Under Armour, Klarna, Alibaba, and Applied Materials

- Bitcoin hovered around $81,332, consolidating near the $80,000 threshold

Last week concluded with U.S. equity markets establishing new record territory. The S&P 500 advanced 0.84% to finish at 7,397.09, while the Nasdaq surged 2.35% to close at 29,195.16. The Dow Jones Industrial Average posted a marginal 0.02% gain, highlighting technology’s leadership role in the latest rally.

April’s employment data provided reassurance to market participants. Nonfarm payrolls expanded by 115,000 positions, significantly exceeding the consensus forecast of 55,000. The jobless rate remained unchanged at 4.3%. These robust figures alleviated concerns about labor market deterioration while simultaneously diminishing expectations for imminent Federal Reserve interest rate reductions.

The 10-year Treasury note yield declined to 4.33%, accompanied by the VIX volatility index retreating to 17.08. Gold appreciated 1.39% to reach $4,747 per ounce. Crude oil declined 1.79% to $93.38 per barrel, partially influenced by emerging diplomatic signals between the United States and Iran.

Semiconductor equities delivered exceptional performance. Micron skyrocketed nearly 38% throughout the week. Sandisk climbed more than 31%. Intel shares jumped following media reports indicating preliminary agreement to manufacture processors for Apple. Advanced Micro Devices similarly registered gains.

Artificial Intelligence Partnerships Spark Volatility

Anthropic announced plans to leverage SpaceX’s Colossus supercomputer infrastructure to enhance capabilities for its Claude AI platform. Akamai shares rallied dramatically following reports of a $1.8 billion cloud infrastructure agreement with Anthropic. Nvidia disclosed intentions to invest up to $2.1 billion developing as much as 5 gigawatts of AI computing infrastructure.

Not all AI-related companies experienced positive momentum. SoundHound declined despite reporting revenue growth. HubSpot retreated following conservative forward guidance. Cloudflare dropped after issuing disappointing second-quarter projections alongside workforce reduction announcements.

Rocket Lab soared 34% following impressive first-quarter financial results and securing its largest launch contract to date. Dell Technologies rallied after President Trump encouraged White House visitors to “go out and buy a Dell.” Spirit Airlines ceased operations following the collapse of emergency rescue negotiations.

Bitcoin concluded the week near $81,332, slipping 0.12%, maintaining proximity to the $80,000 level without establishing decisive directional momentum.

Critical Events for the Coming Week

The April Consumer Price Index report arrives Tuesday morning. Energy price components command particular attention following March’s explosive 20%+ increase. Elevated gasoline costs continue exerting pressure on lower-income household budgets.

April retail sales figures publish Thursday. Apparel retailers and miscellaneous store categories experienced declining sales during the previous reporting period. Quarterly results from Under Armour, On Holding, Birkenstock, and Klarna should provide additional perspective on consumer spending patterns.

Cisco Systems delivers its quarterly report Wednesday after market close. Alibaba announces results Thursday. Applied Materials reports Thursday as well, potentially offering valuable insights into semiconductor equipment demand trends.

The Federal Reserve maintains its position as a central focus. Current labor market conditions appear sufficiently robust to sustain economic expansion, yet insufficiently weak to prompt the central bank toward near-term monetary easing. Treasury yields and Federal Reserve communications will likely continue serving as primary market catalysts throughout the coming sessions.